Funding for future air mobility (FAM) has slowed since its 2021 peak of USD6.8 billion, in line with a broader decline in venture funding for all sectors, according to a report Bridging the gap: How future air mobility can adapt to decreased funding from market analysts McKinsey.

“Total FAM deal value was about USD3.9 billion in 2023, and funding for 2024 is expected to be similar based on year-to-date trends, with nearly USD2.5 billion in funding announced by August.1

“Historically, the majority of FAM funding has been invested in projects related to urban air mobility (UAM), including electric vertical takeoff and landing (eVTOL) aircraft, with surveillance/cargo drones in second place. The remaining funding was allocated to supersonic aircraft, regional air mobility (RAM), or the broader ecosystem. Together, UAM/eVTOL aircraft, surveillance drones, and cargo drones account for nearly 80 percent of publicly disclosed FAM funding received to date in 2024.

“The major drop in UAM/eVTOL funding comes at a particularly bad time for companies in this segment. Some leading eVTOL companies are getting close to commercialization, with about a dozen already flying full-scale prototypes and some testing conforming aircraft as part of the certification program. AutoFlight and EHang have already received type certification for their aircraft in China, while others, such as Archer and Joby, are targeting certification within the next 18 months. Yet most of the players will require additional funding to complete the development, prototyping, and testing required for type certification, which typically requires USD1 billion to USD2 billion.”

“eVTOL players will also need funds to develop manufacturing and supply chain capabilities, which are often quite capital intensive, and companies planning to operate aircraft will need capital to build or acquire their initial fleet, particularly in the beginning, when the aircraft are still unproven and thus unsuitable for the asset-backed financing frequently employed for established aircraft models. Aircraft-manufacturing programs tend to be both margin- and cash-negative for many years post-certification, so the industry-wide funding decline spells a major challenge for eVTOL players.

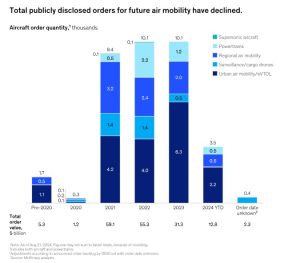

“While the funding decrease is rightfully generating concern across all FAM segments, there are some reasons for optimism. Current FAM orders are still strong—now numbering about 35,500 in total—and are valued at nearly USD168 billion, including options and letters of intent. These figures show that a market exists for FAM aircraft. While order quantities remained largely flat from 2022 to 2023, order value decreased by more than 40 percent. This decline is partly driven by a smaller share of orders for larger RAM or supersonic aircraft and a surge in orders for smaller UAM aircraft.”

For more information

https://www.mckinsey.com/industries/aerospace-and-defense/our-insights/future-air-mobility-blog/bridging-the-gap-how-future-air-mobility-can-adapt-to-decreased-funding

(Image:McKinsey)